Skip full prize with Access Bank POS & Cards

Access Bank cardholders can enjoy exciting discounts across restaurants, hotels, and

more when they pay with their cards on Access Bank POS terminals at select merchant locations

ACCESS BANK CREDIT CARDS

The Access Bank Credit Visa card is a dual-currency denominated

payment card which allows you spend and settle in naira for

domestic transactions while all your international transactions

are billed and settled in US dollars.

ACCESS BANK DEBIT CARDS

The Access Bank Credit Visa card is a dual-currency denominated

payment card which allows you spend and settle in naira for

domestic transactions while all your international transactions

are billed and settled in US dollars.

ACCESS BANK DEBIT CARDS

The Access Bank Credit Visa card is a dual-currency denominated

payment card which allows you spend and settle in naira for

domestic transactions while all your international transactions

are billed and settled in US dollars.

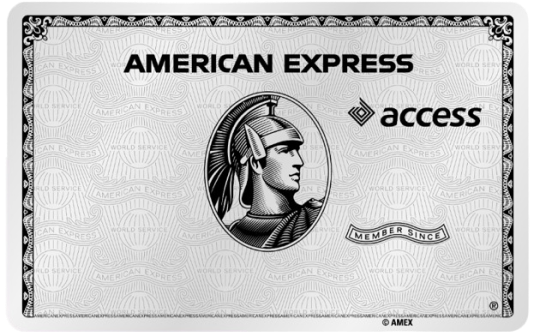

AMEX GOLD CARD

Introducing the Access Bank

American Express® Gold Card.

AMEX PLATINUM CARD

Introducing the Access Bank

American Express® Platinum Card.

| Products | Limit | |||

|---|---|---|---|---|

| ATM | POS/WEB | |||

| Local | International | Local | International | |

| Visa Naira Debit Card – Tier 1 & 2 | N40,000 | Not Available | N2,000,000 | Not Available |

| VISA CLASSIC CARD | N40,000 | Not Available | N2,000,000 | Not Available |

| VISA PRIVILEGE CARD | N40,000 | Not Available | N5,000,000 | Not Available |

| VISA PLATINUM CARD | N40,000 | Not Available | N2,000,000 | Not Available |

| VISA SIGNATURE CARD | N40,000 | Not Available | N2,000,000 | Not Available |

| Visa Business Debit Card | N40,000 | Not Available | N5,000,000 | Not Available |

| MasterCard Debit Card | N40,000 | Not Available | N2,000,000 | Not Available |

| VERVE | N40,000 | Not Available | N2,000,000 | Not Available |

| Card Types | Limit | |||

|---|---|---|---|---|

| ATMS | POS | |||

| Local | International | Local | International | |

| Visa prepaid Card | N40,000 | Not Available | N2,000,000 | Not Available |

| Mastercard Prepaid | N40,000 | Not Available | N2,000,000 | Not Available |

| Verve Prepaid Card | N40,000 | Not Available | N2,000,000 | Not Available |

| Card Types | Limit | |||

|---|---|---|---|---|

| ATM | POS/WEB | |||

| Local | International | Local | International | |

| USD Debit Card | Not Available | $1,000 Daily | Not Available | Unlimited |

| Travel Card | Not Available | $1,000 Daily | Not Available | Unlimited |

| USD Credit Card | Not Available | $1,000 Daily | Not Available | $10,000 Daily |

| Card Types | Limit | |||

|---|---|---|---|---|

| ATM | POS/WEB | |||

| Local | International | Local | International | |

| Platinum Card | Not Available | $2,000 Daily | Not Available | $50,000 |

| Gold Card | Not Available | $1,000 Daily | Not Available | $20,000 |

| Card Types | Limit | |||

|---|---|---|---|---|

| ATMS | POS | |||

| Local | International | Local | International | |

| NGN Credit Card | N40,000 | Not Available | N200,000 | Not Available |

| USD Credit Card | Not Available | $1,000 Daily | Not Available | $10,000 Daily |